| 000 Template | Sample Docs Form Flow to 2024 Info 2023 Info 2022 Info ATX LACERTE |

| 529 Plan Contributions | – Not deductible on Federal taxes – Each State has it own plan – For Federal, Earnings in 529 plan grow tax-deferred and are not taxed upon withdrawal when used to pay for qualified education expenses New York 529 Plan Contributions Form NY IT-203, line 29 Note: Amount will show in Federal amount column only Lacerte Info: 1. Add New York as state in Screen 1 2. Go to Screen 51 -Modifications, select New York, then in Sections select New York Subtractions. 3. Enter amount in S-103 College tuition savings deduction 3a. Year 2023: amount limit is $5,000 single, $10,000 MFJ |

| 529 Plan Distributions Expenses, Losses | To report 529 plan expenses on your taxes: – You receive Form 1099-Q and/or Form 1098-T, which will list the amount of the 529 plan distribution and how much you used to pay for college tuition and fees, but it is up to you, the 529 plan account owner, to calculate the taxable portion. You can write off Losses – If you close the account, withdrawing all the funds, the investment loss is deductible as a miscellaneous itemized deduction on Schedule A. Transfer to Roth IRA – Starting 2024, under certain circumstances, 529 account holders can transfer up to a lifetime limit of $35,000 to a Roth IRA for a beneficiary |

| 568 – LLC Limited Liability Company Single Member LLC Multiple Members LLC CA LLC Fee 800 franchise tax | Single Member LLC 1. Income and Expenses reported on Schedule C of 1040 (Personal) return. 2. Federal – For Single Member LLC, no tax return to file; disregarded entity per IRS. 3. State – not all states require you to file return. Multiple Members LLC 1. IRS treats multi-member LLCs the same as partnerships, unless it files Form 8832 and affirmatively elects to be treated as a corporation. 2. Therefore, when filing taxes, a multi-member LLC must file a Form 1065 Partnership Return (unless elected to be treated as Corporation, then file Form 1120-S). And, K-1 Statement is issued to each partner. 3. 1065 is an informational return only, as the tax liability will pass to the individual members on their personal tax returns. ——————— California – requires you to file Form 568 1. Annual LLC Fee (Info): based on total income from all sources derived from or attributable to California. Typically Gross Income from schedule C is used to determine how much your LLC Fee will be. If gross income < $250,000 then fee is $0. gross income between $250,000 and $499,999 then fee is $900, starting 2001. a. Fee Schedule – CA FTB b. Fee Schedule – Turbotax 2. Annual LLC Tax (info): is $800 due April 15 of tax year. Example for tax year 2024 (1/1/2024 to 12/31/2024), $800 due April 15, 2024. $800 is deductible on Schedule C. 3. Annual LLC Tax Waiver Expired 12/31/2023 (Info). Starting 1/1/2024 all companies must pay the $800 annual tax. a. General Partnership do NOT pay $800 — Info b. Limited Partnership do pay $800 4. 15 Day Exception – info If started business in last 15 days of December (i.e., started after December 17th) AND you did NO business, you do not have to pay the $800 annual tax for that year. 5. Cannot Deduct CA Annual Franchise Fee $800 on California Tax Return a. Lacerte – Enter $800 in Screen 51.011; Tab=St Mod. Section= Income Adjustments, Field =Other Additions b. Flow to Sch CA, page 2, line 8z Texas 1. No annual tax return, but must file Texas LLC Franchise Tax 2. Taxpayer ID number lookup (needed to file LLC franchise tax) ——————— States that Requires You to File Return – Pay Franchise Taxes States are: Alabama, Arkansas, California, Delaware, Georgia, Illinois, Louisiana, Mississippi, Missouri, Minnesota, Nevada, New Hampshire, New York, North Carolina, Oklahoma, Tennessee, Texas, Vermont, and the District of Columbia. |

| 568 – LLC Tax Vouchers CA LLC Voucher | Current Year Voucher – Form 3588 (California) Next Year Voucher – Form 3522 voucher a. for California $800 annual payment – Form 3536: Estimate Fee (paid in addition to $800 annual fee) a. used during tax year to pay California next year’s LLC tax. Use this form only if income is $250,000 or more. Amount of tax is based on gross income. |

| 568 – Single Member LLC Enter on Individual Return (1040) | Use for Single Member LLC only Confirm single member: Form 568, p2, K, max # members should be 1 ——LACERTE info —— 568 Enter on Individual 1040 1. Add California as State return 2. In 1 (Client Info), be sure to check to e-file California LLC 3. Go to 54 (Taxes) 4. In left section, select California SMLLC 5. In top section, for Form, select Schedule C and select activity name 6. LLC name, address and income is auto taken from Schedule C. 7. Section California Single Member, enter… a. CA secretary of state number b. Set Initial or Final return, if any c. Sent Amended Return d. Override amount taxes paid View Return Go to Forms, CA SMLLC If Multiple LLCs for Individual Return (Lacerte Info) 1. Section California Single Member LLC, scroll down to Additional Linked Business. 2. In Form column, select other businesses; and set activity number File Extension for LLC Section California Single Member LLC, scroll down below additional linked business, to Extension. Check box File Form 3537. —— ATX —— 568 Created Using Partnership (yes single member use partnership) 1. Select Partnership/LLC/LLP 2. Enter Company Name, … 3. State Info tab: State =CA, Form =CA 568 Limited Liability Company Return of Income 4. You will have 1065 and Sch K-1 Forms; you can leave them. You will only e-file the CA form. 5. Once finish enter info, exit then re-open return, so all info gets set. |

| 568 – Multiple Members LLC Enter as Partnership (1065) | – Multiple Members LLC is NOT a disregarded entity. It is a partnership. – Multi-member LLC file a partnership tax return AND prepare Schedule K-1. Each member of LLC receives a K-1. ——LACERTE—— 568 is entered as Partnership – Enter total sales on Schedule 1W LLC, line 5. a. get total sales from 1040, Schedule C, line 1, gross sales (not net sales) – C/O (in care of) = 37, Section =CA Misc Info, Field =Additional Info for address. (or, from menu, State & Local; 37 Misc Info; California) – Mark as Final Return ATX: CA 568, Data, check box Final. The word “Final” and the number 1, show at top of 568 form, below address. Lacerte: 37, Section =CA Miscellaneous Info, near top, enter 1 for Final return. The word “Final” and the number 1, show at top of 568 form, below address. – Mark as Initial Return ATX: CA 568, Data, check box Initial. The word “Initial” and the number 1, show at top of 568 form, below address. Lacerte: 37, Section =CA Miscellaneous Info, near top, enter 1 for Initial return. The word “Initial” and the number 1, show at top of 568 form, below address. |

| 592 CA 592 | CA 592 – Resident and NonResident Withholding Statement 1. Non-real estate withholding; for any withholding other than real estate 2. Withholding can be for trust distribution, estate distributions, rents or royalties, independent contractors, etc… see 592 form for list of income. 3. Submitted by Withholding Agent (entity, business, person that withheld the money) to CA FTB. 4. Withholding Agent also sends a 592-B to each entity, business or person that it listed on 592. I.E., Withholding Agent sends 592-B to each entity, business, person from which it withheld money. 5. Entity, business, and person… they are to report the withholding on their tax return. |

| 592-B CA 592-B | CA 592-B – Resident and NonResident Withholding Tax Statement 1. For Entity, business or person (called payee) that had money withheld from them. Form 592-B states how much was withheld. 2. Entity, business or person report withholding on their tax return a. Individual – enter on CA WHWKST, select 592-B Report on California tax retun as follows: For Individual — report on CA 540, p3, line 73 For 1041 (trust) — report on CA 541, p1, line 31 For 1120-S — report on CA 100S, p2, line 33 For 1120 — report on CA 100, p2, line 33 For 1065 — report on CA 568, p1, line 11 Lacerte Instructions – info 1. Go to Screen 55, Part Yr./Nonres. Information. 2. Select California Real Estate & Other Withholding from the top left navigation panel.This will take you to Screen 55.012, California Withholding. 3. Locate the General Information section. 4. Enter a 1 in the 1=592-B, 2=593 field. 5. Scroll down to the Withholding Agent section and complete any applicable fields. 6. Scroll down to the Withholding (Form 592-B) section. 7. Enter the Total amount subject to withholding, if applicable. 8. Enter the Total CA tax withheld, if applicable. 9. Enter the Total backup withholding, if applicable. 10. Click Add in the left navigation panel to enter a second Form 592-B and repeat steps 3-9, if applicable. |

| 592-PTE CA 592-PTE | CA 592-PTE – Pass-Through Entity Annual Withholding Return 1. Use to pass withholding from Withholding Agent (entity, business, person that withheld the money) to another entity, business, person. 2. Submitted by Withholding Agent to CA FTB. 3. Withholding Agent also sends a 592-B to each entity, business or person that it listed on 592-PTE. I.E., Withholding Agent sends 592-B to each entity, business, person from which it withheld money. 4. Entity, business, and person… they are to report the withholding on their tax return. 592-PTE Sample Form (a) on top line, only need to enter the number of payees. Leave all other boxes unchecked. (b) Part I – is the trust (or entity, business, person) that is distributing money to beneficiaries. (c) Part II – is the company that collected the money. On last line, “Amount of Tax Withheld”, is the total amount of money withheld. (d) Part III – is the total amount of money withheld (e) Schedule of Payees are the beneficiaries. Total beneficiaries amount must equal to amount in Parts II and III. |

| 593 CA 593 | CA 593 – Real Estate Withholding Statement 1. For real estate withholding only 2. Submitted by Escrow Company to CA FTB 3. Escrow Company provides copy to seller 4. Seller report withholding on their tax return For Individual — report on CA 540, p3, line 73 For 1041 (trust) — report on CA 541, p1, line 31 For 1120-S — report on CA 100S, p2, line 33 For 1120 — report on CA 100, p2, line 33 For 1065 — report on CA 568, p1, line 11 |

| 843 | IRS Request for Abatement | IRS Info Inside tip. For California, you can fax form to Fresno fax # 855-230-1160 although IRS say to mail form, you can fax to this number. Then call IRS account services in 2 weeks later to see form processed. |

| 8915-F | Qualified Disaster Retirement Plan Distributions and Repayments. Form 8915-F replaces Form 8915-E for 2021 and later years. Flow to ——LACERTE—— 1. Go to Screen 13.1 Pensions, IRA Distributions. 2. Enter the information from the 1099-R. 3. Select the Section for Form 8915 (Qualified Disaster Relief for Retirement Plans). 4. Check the box for the appropriate tax year of the qualified disaster. 5. Complete the required information. |

| 990 / 990-EZ Exempt Org | ——LACERTE—— C/O (in care of) = 65, Section = CA Misc Form 199; Field =Additional & Supplemental address info. (OR, State & Local; 65 Misc Info; California) Year of Formation = 1, Section =Return Info, Field =Year of Formation Mission Statement = 35 – Schedule O – Part III, line 28, click on amount and jump to; enter in “Exempt purpose achievements” – also in wording above line 28 Detail / Pro Serv Acc |

| 990-PF | Form 990-PF is the annual tax return used by private foundations exempt from income tax. |

| 1040-SR | Form 1040-SR is a large-print version of Form 1040 that is designed for taxpayers who fill out their tax return by hand rather than online. A standard deduction table is printed right on the form for easy reference. You need to be 65 or older to use Form 1040-SR. You can use all IRS schedules (additional forms) with Form 1040-SR, including Schedules 1, 2, and 3, to report information not directly reported on Form 1040-SR |

| 1041 Trusts Estates, Fiduciary | – Brokerage Fees / Investment Advisory Fees – Not Deductible (IRS Info) |

| 1042-S | Flow to 1040-NR Used to report various types of income paid to nonresidents in the US. Or, foreign person that gets U.S. income that is subject to withholding. Lacerte: 1. 58.2 2. Enter info using 1042-S form |

| 1065 Partnership Return Review Return for last year ending balances | Special Allocation Depreciation – Real Estate A special allocation is a financial arrangement that is set up in a partnership or LLC that restructures the manner in which profits and losses are distributed to the owners or partners in a way that does not correspond to their actual percentage interests in the business. Lacerte Info 1. This is “Other Deductions” 1065, p4, line 13d 2. In this case, the other deduction is a special allocated depreciation 3. Depreciation is allocated to Schedule K-1, box 13, code W 4. Depreciation does not go on 8825 5. It’s a special allocation, because the allocation percent is different from partnership percentage Note: when entering allocations in 29 (Special Allocations), it takes time for the system to update amounts in box 13, code W Tax Return Review 1. Make sure last year ending balance is the current year beginning balance and print forms for: 7203, Schedules L, M-1 and M-2 Special Allocation – Cash and Marketable Securities Lacerte Info |

| 1098-T Tuition Statement American Opportunity Tax Credit (AOTC) Life Time Learning Credit (LLC) | Form 8863 — flow to 1040, Sch 3, p1, line 3 If Scholarship is Taxable: flow to 1040, Sch 1, p1, line 8r ATX: Enter on 1040 EdExp (1098-T) Lacerte: 38.1 Box 1 = total tuition costs and fees paid during the tax year Box 2 = blank, not used Box 3 = blank, not used Box 4 = school adjusted expenses for previous year. If it turns out a previous year’s expenses were lower than initially reported, student may need to file amended return and may own taxes for that year. Box 5 = total scholarships awarded. Scholarships amounts were paid directly to the school for the student expenses. Box 6 = shows any adjustments the school has made to scholarships and grants reported on a previous year’s 1098-T. These adjustments may affect the student’s tax liability for the previous year, so the student may have to file an amended return. Box 7 = this box is checked if the amount in Box 1 or 2 includes expenses for an academic term that begins in the first three months of the year following the year covered by the 1098-T. Box 8 = indicates that student is enrolled at least half time Box 9 = indicates student is enrolled in a graduate program Box 10 = When an insurer reimburses a student’s expenses, it provides that student with a copy of the 1098-T. Box 10 is used to show the amount reimbursed. ——————————— Scholarship is taxable income = Amount in Box 5 (scholarships) is GREATER THAN the amount in Box 1 This means you cannot use any expenses to reduce your tax bill. You must report the excess as taxable income on the federal return. Scholarship is NOT taxable, so can use expenses as a deduction or credit = Amount in box 5 is LESS THAN the amount in Box 1. So, Subtract Box 5 from Box 1 (or Box 2); then report that amount on taxes. ——————————– LACERTE Scholarship is taxable income 1. Box 5 amount is Greater Than Box 1 2. Taxable Amount = Box 5 minus Box 1 3. Enter Taxable Amount in: 14.1 / Alimony and Other Income / Taxable Scholarships and fellowships. — flow to 1040, Sch 1, p1, line 8r Scholarship is NOT taxable income, so deduct expenses 1. Box 5 amount is Less Than Box 1 2. Deduct Expenses Amount = Box 1 minus Box 5 3. Enter Deduct Expenses in: 38.1 a. Enter Student Information b. Enter American Opportunity Credit (AOC) Disqualifiers, if any c. Enter Educational Institution d. Current Year Expenses: d1. Enter Deduct Expenses Amount in Qualified tuition and fees (net of nontaxable benefits) d2. Books and supplies required to be purchased… = get info from student d3. Books and supplies not entered above (AOC only) = other expenses 4. Flow: Form 8863, which flow to 1040, Sch 3, p1, line 3 ——————————- FAQs IRS Info – American Opportunity Tax Credit (AOTC) 1. How many years can you claim American Opportunity Credit? 4 years 2. What is the credit amount? Max credit is $2,500 per year. If the credit brings the amount of tax you owe to zero, you can have 40 percent of any remaining amount of the credit (up to $1,000) refunded to you. 3. Can Graduate Student claim AOTC cedit? no? may can claim the Lifetime Learning Tax Credit IRS Info Life Time Learning Credit IRS – Compare AOTC vs LLC More 1098-T info Can Claim Post secondary (College Credit) for Either: 1. The American Opportunity Credit, part of which may be refundable. 2. The Lifetime Learning Credit, which is nonrefundable. NOTE: Student may have to get copy of form from school, because school don’t always send them to the students. Who Enters 1098-T Parent or Student? If the parent is claiming the student as a dependent on their (the parents) income tax return, then the parent enters the 1098-T Tuition form on their (the parents) income tax return. If You have a Business, and you do not receive 1098-T, you can deduct education expenses on Schedule C. However, you must be getting an education to improve your skills for your business. You can Deduct – Tuition, books, supplies, lab fees, equipment, and similar items – Certain transportation and travel costs – Other educational expenses, such as the cost of research and typing You can NOT Deduct – College Application Fee – Parking – Room and board, or other living expenses – Student health fees and other medical expenses – Transportation – Insurance, including property or renters insurance for college students – Expenses for sports, games, or hobbies, unless they’re necessary for your degree program – The cost of non-credit courses, unless necessary for your degree program (the LLC may include these costs if they’re for a career development course) American opportunity tax credit (AOTC) IRS Requirements | Who Can – Can’t Claim Credit | Comparison / Easy List 1. Can deduct up to $2,500 2. must receive form 1098-T 3. be pursuing a degree or other recognized education credential 4. be enrolled at least half time for at least one academic period* beginning in the tax year 5. Not have finished the first four years of higher education at the beginning of the tax year 6. Not have claimed the AOTC or the former Hope credit for more than four tax years 7. Not have a felony drug conviction at the end of the tax year 8. If married, you cannot file separate return |

| 1098-T Tuition – Self Employed | Deduct “Qualifying Work-Related Education” on Schedule C You Can Deduct Tuition, books, supplies, lab fees, transportation to and from classes and related expenses. You must be able to prove that the course: 1. Maintains or improves skills you need in your trade or business 2. Is required by law or regulation for keeping your license to practice in your trade or profession You can’t deduct education expenses you incur: 1. To meet the minimum requirements of your present trade or business 2. That qualify you for a new trade or business |

| 1099 – ATX Payroll | Print Single 1099 1. Click Detail tab; on left in Print column, put ‘X’ in only the 1099 you want to print; click print Add another 1099 to an already accepted e-file 1. You cannot add to an accepted e-file. 2. Instead, you can duplicate the existing company, go to detail tab, delete all 1099 recipients, then add new recipients. create e-file, then transmit |

| 1099-B Stock Sale Computershare see also Restricted Stock Unit | Flow to 8949 and Schedule D, which flow to 1040, line 7 (Capital gain or loss) Enter: Form 8949, tab = input Covered Transactions (covered securities) = broker is required to report cost basis to both taxpayer and IRS Noncovered Transactions = broker only send cost basis to taxpayer. However, taxpayer should report on tax return. Because cost basis is subtracted from sale price (proceeds), which lowers taxed amount. ——LACERTE—— Enter: 17 Dispositions (or Detail / Income / Dispositions) for Various, enter negative date; ex: -01/01/2022 Gain or Loss = N/C, then make cost basis same as proceeds Gain or Loss = N/A, then make cost basis same as proceeds Cost Basis = N/A, then enter cost basis same as proceeds When Gain or Loss is not determine, make cost basis same as proceeds so net effect is zero gain/loss. Sales Proceeds not provided – for K-1 when sales proceeds not provided, enter zero for sales proceeds, which makes the transaction a loss – client need to call their broker for the info ??? – can happen on K-1 that has a 8949 Cost basis is the price paid to acquire shares, plus commissions and any fees. Cost Basis is Zero (example) Check for code to see if supplemental info is provided. If provided use cost basis info from supplemental. If not provided you will have to ask client or look at past returns. Cost Basis is Partially Provided (example) Taxpayer will have to get info for their broker or find stock purchase document, which should show purchase price |

| 1099 Distributions and Charges | Limited Partnership Income 1. Enter on Schedule K-1 Non-Reportable Dividends and Interest Non-Reportable Tax-Exempt Interest Taxable Muni Accrued Int. Paid Non-Tax Muni Accrued Int. Paid 1. Enter on 1099-INT 2. Create New Record 3. Enter in Tax-Exempt Interest, Total municipal bonds Other Accrued Interest Paid Flow to Schedule B -Interest and Ordinary Dividends 1. Enter on 1099-INT (interest income), 2. Go to Adjustments to Federal Taxable Interest, enter in Accrued Interest Margin Interest 1. Enter on Schedule A, Investment Interest 2. You can’t deduct more margin interest than your net investment income. 3. Your net investment income will cap your margin interest tax deduction for the current tax year. For example, say your investments gave you a net investment income of $1,000, and you have $5,000 of margin interest to deduct from your taxes. However, you can only deduct up to your net investment income for the year ($1,000). Therefore, you can deduct $1,000 of margin interest for this year’s taxes and carry over the remaining $4,000 to future years. Non-Reportable Distribution Expenses Excess Bond Premium Additional Bond Premium |

| 1099-DIV 1099-DIV California | Box 1a – Total Ordinary Dividends a. flow to 1040, line 3b Box 1b – Qualified Dividends a. flow to 1040, line 3a b. the portion of box 1a that is considered to be qualified dividends Box 2a – Total Capital Gain Distributions a. flow to 1040, Schedule D, line 13; AND to 1040, line 7 b. capital gain distribution from your investments; e.g., mutual fund distribute capital gains to you Box 2b – Unrecap Section 1250 Gain a. flow to Box 2d – Collectibles (28%) Gain a. flow to Box 2e – Section 897 Ordinary Dividends a. flow to Box 2f – Section 897 Capital Gain a. flow to Box 3 – Non-Dividend Distribution a. flow to Box 4 – Federal Income Tax Withheld a. flow to 1040, p2, line 25b b. federal taxes withheld from your distributions. Box 5 – Section 199A Dividends a. flow to 8995, line 6 Box 6 – Investment Expenses a. flow to CA, Sch CA, p6, line 21 other expenses: investment, … Box 7 – Foreign Taxes Paid a. flow to Schedule 3, p1, line 1 b. if date not provided, enter year end date , ex: 12/31/2023 c. must add form 1116 (Lacerte 35) d. Foreign Source Income is Ordinary Dividends (also called non-qualified) ….. Ordinary Dividends = Total dividends and distributions i.e. all dividends i.e. = non-qualified (ordinary) + qualified + section 199A + long term capital gain, … e. Foreign Qualified Income is Qualified Dividends ….. Qualified Dividends = Qualified Dividends f. Foreign Capital Gain is 30% for Long-Term and Short-Term Foreign Capital Gain Distributions – Example (scroll to one with capital gain) ….Add Long-Term and Short-Term Capital Gain Amount, then multiply by 30% g. Sample calculate foreign taxes h. Other dividend Info, explanation Box 8b and 8c – if not provided, use same amounts in 1a and 1b Box 9 – Cash Liquidation Distributions (Lacerte Details) a. flow to 8949; Schedule D b. If cost basis is provided, enter box 9 info and cost basis in form 8949, like other 1099-B transactions — check end of 1099 statement for cost basis; maybe in section “Unrealized Cost Basis Information for Securities Subject to Amortization/Accretion…” c. If NO cost basis, Do not enter; since don’t have cost basis. Note: more info This amount is the cash the investor/taxpayer received upon liquidation of all or part of the underlying entity. Generally the cash distribution is considered a return of the cost or basis in the investment. Box 10 – Non-Cash Liquidation Distributions (Lacerte Details) a. flow to 8949; Schedule D b. If cost basis is provided, enter box 10 info and cost basis in form 8949, like other 1099-B transactions — check end of 1099 statement for cost basis; maybe in section “Unrealized Cost Basis Information for Securities Subject to Amortization/Accretion…” c. If NO cost basis, Do not enter; since don’t have cost basis. Note: Liquidating distributions (cash or noncash) are a form of a return of capital. Any liquidating distribution you receive isn’t taxable to you until you recover the basis of your stock. After reducing your stock’s basis to zero, you’ll need to report the liquidating distribution as a capital gain on Schedule D. Box 12 – Exempt Interest Dividends a. flow to 1040, line 2a a1. CA: Flow to Sch CA, page 1, line 2 b. sample how to calculate c. Lacerte: Enter 12, Section =Tax-Exempt Interest, Field= Total Municipal Bonds d. For In-State Municipal Bonds, d1. California Municipal Bonds are exempt from California (State) Taxes d2. See line 15 State. If a state is listed (ex: CA), then dividends has State exempt interest. I.e., “In State Municipal Bonds” that is exempt from state taxes. d3. If State amount is not provided, you must calculate amount. … To calculate, check pages which contains “Detail for Dividends and Distribution”, or “Reportable Exempt-Interest Dividends”, etc. Look at each name to see if it has in it CA, California or state that tax return is for. — if Percent, multiply by stock amount for each name / company — if Amount, add up all amount with CA in the name Box 13 – Specified Private Activity Bond Interest Dividends a. flow to Form 6251, Part 1, line 2g (Alternative Minimum Tax) b. Lacerte: enter 12, Tax-Exempt Interest, Field = Certain private activity bonds (6251) Box 14 – state withholding Federal Obligations Exclusion US Territories Obligations Exclusions Exclusions from Government Obligations US Bonds sample 1 | sample 2 | sample 3 This amount is being excluded from State taxes. Federal obligations are excluded from state taxes. In most states, fund dividends from interest on direct U.S. government securities are exempt from state and local taxes. 1. Lacerte – enter in 12 – Dividend Income, section Dividend Income, Field = U.S. Bonds (nontaxable to State % or amount) 2. Flow to State. CA, Sch CA, page 1, line 3, Subtractions column (because not taxable to state) Municipal Obligations Exclusion sample 3 1. State Obligations (ex: California) a. Lacerte – enter in 12 – Dividend Income, section Tax Exempt Interest, Field = In-State Municipal Bonds (State % or amount). a1. Max exemption is total of tax exempt interest. b. Flow to State. CA, Sch Ca, page 1, line 3, it reduces the amount in the Additions column. US Government Securities – Example Enter Amount in US Bonds (nontaxable to state) (% or amount) 1. For each Dividend Securities Description, check Supplemental Page to see if it is a US Government Securities. If it is, get the percent. You will mulitply the percent times the securities’ description amount. 2. US Bonds amount = Percent X (Total Dividends & Distributions – Long-Term Capital Gain) NOTE: Subtract long-term capital gain. Do NOT subtract short-term capital gain (short-term capital gain is included) 2a. Add US Bonds amount for each securities and put total in Lacerte Direct Federal Income Direct Federal Obligation 1. Enter amount in US Bonds Indirect Federal Income Indirect Federal Obligation 1. Enter amount in US Bonds Other Info A common reason for receiving a 1099-DIV form is because some of the investments you own paid dividends during the year. You won’t file the 1099-DIV with the Internal Revenue Service, but you will need the information it reports when preparing your tax return. |

| 1099-INT | Flow to Schedule B Interest and Dividends flow to Schedule B ref: Buetow, Mac 13 – Bond Premium on Tax-Exempt Bond 15 – State (CA) a. If 13 has an amount and CA (or State) is shown in 15, check if any of the bond premium is exempted by the State. b. Add “Tax-Exempt Interest From California” AND “Bond Premium From California”. note : bond premium from california is a negative number. Enter result in 1099-INT, Tax-Exempt Interest, In-State Municipal Bonds. |

| 1099-K | If Sold Personal Items and receive 1099-K Sold at Loss: 1. Report Income received from sale on Schedule 1, line 8z 2. Report Price you paid for item on Schedule 1, Part II, line 24z Or you can 1. Report Income received from sale on form 8949 Sold and Made Profit (your profit is taxable) 1. Report on form 8949 You Received 1099-K In Error (i.e., money given to you by friends and family) If you cannot get corrected 1099-K from issuerer. Then you need to report the income; and you can enter adjustment. 1. Enter Income Schedule 1, line 8z 2. Enter Adjustment on Schedule 1, line 24z, which nets to zero |

| 1099-LTC | Sample Flow to Form 8853 Lacerte (info) 1. 32 (HSA/MSA/LTC Contracts) 2. Enter according, look at box 3 to determine where to enter box 1 amount. Also look at box 5 for type of illness |

| 1099 Correcting ATX Correct 1099 ATX Correcting 1099 ATX | Correct 1099s After It has been Accepted in ATX Info | Info2 search =correct 1099 You MUST correct the original accepted return. You cannot correct a copy / duplicate return. 1. Save copy of the original return so that you have your original amounts a. select return, then click Returns menu and select Duplicate Selected Return. You can name is original 2. Edit Original accepted return. Go to each person that needs correcting, check box Corrected, and change info. I.e., enter new info over existing info 3. On the E-file menu, click Create E-file. 4. In the Create E-file box, check the Federal 1099 Corrected box. 5. Click Create. The Corrections Confirmation window opens, listing all recipient records that you changed since the IRS accepted the original e-file. 6. Mark each record you want to include in the corrected e-file, or click Select All to mark all records shown. 7. Click Create. 8. Click OK. 9. If the Correct E-file Errors window appears, click Continue and then correct the errors. After making the necessary corrections, repeat the e-file creation process. 10. Transmit the corrected e-file. |

| 1099-NEC 1099-MISC 1099 Filings 1099 IRS Free Filing 1099 IRS Filing | If Receive, Report on Schedule C Issued to Vendors: Based on Calendar Year 1. 1099 is issued based on Calendar year. It is NOT based on fiscal year. 2. Even though your company’s tax year straddles 2 calendar years, the 1099-misc and nec forms must be filed on a calendar year basis. 3. Therefore, report payments made during calendar year. Do not report payments made in a different year. Self Employment Tax 1. Applies to all 1099 income over $400 2. Report 1099 Income on Schedule C Rent Paid 1. Send a 1099-MISC for rent paid if rental income paid to an individual or business exceeds $600 during a calendar year. 2. The payment is for services related to rental properties, including office or commercial space. 3. Property management companies must send a 1099 for rent to the property owner. 4. Renting to a family member does not require a 1099. Who Receives 1099 Anyone receiving payment for service over $600 that is one of the following: 1. Single Member LLC 2. Multiple Member LLC 3. Partnerships 4. Limited Liability Partnerships (LLPs) taxed as Partnership 5. Trusts 6. Estates 7. Lawyers, even if lawyer or law firm is a corporation NOTE: Issue 1099 to vendor that provides a service. Purchasing a product is not providing a service. Info Who Do NOT Receive 1099 1. Corporations (1120, 1120-S (s-corp)); except law firm always get 1099 2. LLC Electing to be taxed as S-Corp or Corporation E-Filing Required if submitting more than 10 1099s You must e-file if you have ten or more 1099s IRS E-File System (Free) | Information Returns Intake System (IRIS) Info – Can file online Free. – Will need to setup IRIS Taxpayer Portal account. – To use the IRIS Taxpayer Portal, you need an IRIS Transmitter Control Code (TCC). This 5-digit code identifies your business when you e-file forms. It can only be used for IRIS. – You can apply for IRIS TCC for a. your business only (issuer), b. your business and others (transmitter) c. software developer |

| 1099-MISC Split Income with Another Person | 1040: for for Misc Income Split with Another Person 1. Enter full amount from 1099 (INT, DIV, MISC, etc) on 1099 form 2. Enter 1/2 the amount as other income; enter as negative number (to subtract from income); put the description as “Nominee Adjustment”. I.e., 1040, line 8 (other income), click arrow, Sch 1, line 8z, click arrow, description is “Nominee Adjustment” and enter amount as negative number. |

| 1099-MISC Rent Box 1 | info If you own property that is rented to a business and you receive a 1099-MISC with the amount of rent paid to you reported by the business in box 1, you should report the amount on Schedule E of Form 1040 as passive activity income If you’re in the business of renting personal property, you should report income and expenses related to personal property rentals on Schedule C (Form 1040) If you’re not in the business of renting personal property, you should report the rent as other income; 1040 line 8. |

| 1099-MISC Other Income | Flow to Form 1040, Schedule 1, line 8 ——LACERTE—— 1. 14.1 (SS Benefits, Alimony, Miscellaneous Income) 2. In section Alimony and other Income, Field =Other Income |

| 1099-MISC Royalties Box 2 | Enter on Schedule E If for Oil & Gas – deduct depletion expense; which is typically 15% of the amount in box 2. — In Lacerte, enter on Schedule E, section Oil & Gas, field is Production type (at top of oil & gas section) |

| 1099-OID Original Issue Discount | IRS Form Flow to Schedule B see Lacerte explanation reference Christian and Julia Will, Morgan Stanley account xx8682 ref Gus Christopoulous OID Box 1 – Original Issue Discount a. enter on 1099-INT b. Lacerte: 11, Bank, S&L, etc; c. flow to 1040, p1, line 2b (taxable interest) OID Box 2 – Other Periodic Interest a. enter on 1099-INT b. see Lacerte explanation on where to enter c. flow to 1040, p1 line 2a (if tax exempt – municipal bonds) OR 2b (if taxable interest) OID Box 3 – Early withdrawal penalty a. enter 1099-INT b. Lacerte: 11, scroll down to Other, enter in Early withdrawal penalty c. flow to 1040, Schedule 1, p2, line 18 OID Box 4 – Federal Income Tax Withheld a. enter 1099-INT b. Lacerte: 11, scroll down to Tax Withheld / Federal Income Tax Withheld c. flow to 1040, p2, line 25b OID Box 5 – Market discount a. enter on 1099-INT b. Lacerte: ??? c. flow to ??? OID Box 6 – Acquisition premium a. enter on 1099-INT b. Lacerte: 11, section Adjustments to Federal Taxable Interest, Field = Original Issue discount (OID) b1. If there’s an amount in both boxes 6 (acquisition premium) AND 11 (Tax exempt original issue discount), enter Acquistion premium in Total Muncipal Bonds; AND enter Tax Exempt Original Issue discount in Amortizable bond premium on tax-exempt bonds. — Add new Interest record, to enter info, add “OID” to payer’s name; to identify record as OID. c. flow to OID Box 8 – Original issue discount on U.S. Treasury obligations a. enter on 1099-INT b. Lacerte: 11, enter in U.S. bonds, t-bills (nontaxable to state) or can enter in Banks, S&L, etc. c. create new line, name ex: schwab 1099-OID d. flow to 1040, line 2b (taxable interest) OID Box 9 – Investment expenses a. enter on Schedule A, Misc Ded Subject to 2% AGI limitation, Investment Expense b. Lacerte: 25, Misc Ded. Subject to 2% AGI limitation, investment expense c. flow to Sch CA, p6 line 21 OID Box 10 – Bond Premium a. enter on 1099-INT b. Lacerte: 11, enter in Banks, S&L, etc. c. create new line, eame ex: schwab-bond premium d. flow to 1040, line 2b (taxabel interest) OID Box 11 – Tax Exempt OID a. enter on 1099-INT b. Lacerte: 11, Adjustments to Federal Taxable Interest . Original Issue Discount (OID) c. flow to ??? ATX Support | atx support Enter using form 1099-INT. Enter in Box 1; AND in the adjustment to box 1; enter amount and code (code O?) |

| 1099-Q | Form 1099Q Worksheet | Sample Document You are the designated beneficiary of a 529 plan or a Coverdell Education Savings Account (Coverdell ESA). 1. If taxable: taxable amount flow to 1040, Schedule 1, line 8z 2. You don’t need to report if all distributions used for Your qualified education expenses. 3. If you did not use the money for Your education, then the full or adjusted amount on 1099-Q is taxable. (flow to sch 1, line 8z) ——Lacerte—— 1. 14.3 (Education Distributions) 2. Section Qualified Expenses: usually same as gross distributions 3. Section Form 1099-Q: enter Gross Distribution, Earnings, Basis, and set (5) 4. if it should not be taxable, make sure nothing is showing on sch 1, line 8z Tax Cuts Jobs Act (TCJA) expanded the types of expenses a 529 plan can be used to pay. Expenses include: K-12 elementary and secondary school tuition for public, private and religious schools. Previously only Coverdell ESA funds could be used for primary and secondary expenses. You can also you 529 plan to pay for registered apprenticeship programs You can also rollover amounts from 529 plans to ABLE accounts (Achieving a Better Life Experience act of 2014) –tax advantaged savings accounts for individuals with disabilities and their families. |

| 1099-R (Roth IRA Distribution) 1099-R taxable amount unknown 1099-R Unknown Box 2a Unknown | Distribution code = J, means Roth IRA distribution. – distribution may not be taxable. – you can withdraw money you contribute to Roth IRA anytime and without penalty – you can withdraw earnings after age 59 1/2 after owning the account for at least five years. Withdrawing money earlier can trigger taxes and 10% early withdrawal penalty. Roth IRA Basis = total contribution – total withdraws Taxable amount = distribution – Roth IRA Basis; if <=0, no taxes Make Distribution Non-Taxable – scroll down on 1099-R form, check box “Box 7 include codes J or T” – or, Form 8606 enter 0 on line 7; to zero out amount Box 2a UNKNOWN Different ways to calculate taxable amount 1. Taxable Amount = Gross Distrubtion – Employee Contribution 2. Pension exclusion calculator 3. Can use IRS Simplified Worksheet – see Part IV, Page 22 4. Look at prior year return to calculate percentage: box 2a divided by box 1; use same percent this year |

| 1099-R (State has $0 distribution) | State has withholding, but $0 in state distribution. Put amount from 2a in state distribution |

| 1099-R Required Minimum Distribution (RMD) | RMD | IRS FAQs 1. You MUST take the distribution or pay penalty 2024 Penalty is 25%. It reduces to 10% if corrected within two years. 2023 Penalty is 25%. It reduces to 10% if corrected within two years. 2022 Penalty is 50%. 2. Contact company for your 1099-R or corrected 1099-R. RMD Taken Late (taken after December 31) 1. Still take the distribution. It will be reported on your next year’s taxes. So for current tax year, you will not have a 1099-R to report on your taxes. (note: next year you will have double the 1099-R income to report). 2. File form 5329 to get penalty waived for not taking distrubtion on time 3. Lacerte 5329 – Penalty Waiver (Flow to 5329, p2, part IX) a. 41 (Retirement Plan Taxes 5329) b. Section Excess Accumulation in Plan, enter info, explanation (info sample): On January 15, 2024, while collecting documents to give to our tax preparer, taxpayers discovered that for tax year 2023, the required amounts for RMD were not distributed. During the year in question, taxpayers were unaware of the error as taxpayers were provided incorrect information by their financial institution. Upon discovery of the error, taxpayers took immediate and corrective action by taking the distributions on February 2, 2024 in the amounts of $5,000 and $10,000. Taxpayer believes these actions warrant relief under IRC 4974(d). |

| 1099-SA | 1099-SA worksheet – distributions from health savings account (HSA) Note: Contributions to HSA is Form 8889 (Flow to 1040, Sch 1, p2, line 13) ——LACERTE—— 1. 32 (Health Saving Account) 2. Section Distributions, enter info 3. To exclude distribution from being taxed, a. enter amount in box “Qualified unreimbursed medical expenses…” b. enter info in “Amount to exclude from 20% tax…” |

| 1120 Corporation | |

| 1120S S Corporation Tax Return Review Return for last year ending balances | Schedule M-1 – used to reconcile the income (or loss) that the S corporation is reporting on the tax return with the income (or loss) in its accounting records. Not all S corporations are required to complete Schedule M-1. Schedule M-1, Line 8 should equal Schedule K line 18 Schedule M-2 – reports an analysis of the partners’ capital accounts. This Schedule explains the difference between the partners’ capital accounts as shown in the Balance Sheets (Schedule L) at the beginning of the tax year and at the end of the tax year. more info on accumulated adjustment accounts (AAA). 15a Post 1986 depreciation adjustment – info flow from Fixed Assets, Federal AMT column, line AMT/State Adjustment. Info on this line is auto calculated: Federal Current Year Depreciation minus (-) Federal AMT current year depreciation. Look for Alternative Minimum Tax Depreciation Report (not sure if ATX has this report. CCH prosystem fx has this report) Distributions – Prior Years Distribution 1120S, tab= line 16 d – distributions Flow to Sch K-1, K-1 Stmt; and Form, line 16 D Charity / Contributions 1120S, p3, line 12a Tax Return Review 1. Make sure last year ending balance is the current year beginning balance and print forms for: 7203, Schedules L, M-1 and M-2 |

| 3800 General Business Credit | Can Carryforward Credit for 20 years Lacerte 1. Enter Carryover in Screen 34, General Business & Vehicle Credits 2. Section – Business Credit Carryforwrds and Carrybacks (3800) a. Select Type of Credit; enter Carryforwards amount b. For Type of credit check Part III. See line where amount is entered, this is the type of credit Carryforward Credit 1. Check total amount Current Year Credits (this includes credit from prior years): Part 1, Line 6 2. Check total amount Allowed credit for this year: Part 2, Line 17 3. Carryforward = Line 6 minus Line 17 a. If Line 6 is zero, there are NO credits; and therefore nothing to carryforward 4. There should be part IV showing carryforward credit ??? |

| 3921 ISO Disqualifying Disposition ISO DD ISO = Incentive Stock Options | Example 1 | Example 2 (excel) | More Info | When is AMT Calculated Docs Needed (W2, 3921, 1099-B) |Enter 3921 In Lacerte Two Calculations Needed 1. Capital Gains (Form 8949) View Info from The Balance a. enter sale proceeds, cost basis, … b. Sale Proceed – client should have received 1099-B c. Cost Basis – client should have info from when they purchased stock; or when granted options; or when exercised options. 2. Alternative Minimum Tax (AMT) — report on form 6251 a. AMT = fair market value (fmv) – exercise price b. info on form 3921, employee get this form from employer b. report AMT on Form 6251, line 2i c. Calculate AMT when you exercise the option and not sell the stock in the same year you exercised it. Form 3921 1. Pertains to ISO stock sale. 2. It is a form that companies have to file with the IRS when an existing or former employee exercises an ISO. Your employer should also provide you with a copy of this form 3. It helps determine your cost or other basis, as well as your holding period. It provides details like the date of transfer, FMV of the stock, and the exercise price per share. 3. When you dispose of the stock, you’ll receive Form 1099-B, Proceeds From Broker and Barter Exchange Transactions. This needs to be reported on your tax return. Reporting a Qualifying Disposition of ISO Shares The gain should be reported on Schedule D and IRS Form 8949. The gross proceeds from the sale are required. This information is provided by the broker on Form 1099-B. Other Info 1. Fidelity 2. ISO cannot be transferred to another person or donated to charity. 3. The word “disposition” is just another way of saying that you have sold, gifted, or transferred ownership of your shares. 4. Qualifying dispositions (more info) occur when shares are held for the required holding periods — which means you get capital gain treatment 5. Disqualifying dispositions occur when shares are not held for the required holding periods — which means you do NOT get capital gain treatment. You pay ordinary income on profit. 6. The key distinction between Form 3921 and Form 3922 lies in the type of stock transactions they report. Form 3921 focuses on ISOs, while Form 3922 pertains to ESPPs. |

| 5405 Home buyer credit Home buyer tax credit First time home buyer credit | 2024 (IRS Info) You must file Form 5405 with your 2024 tax return if you purchased your home in 2008 and you meet either of the following conditions. You disposed of it in 2024. You ceased using it as your main home in 2024. 2024 is the last year to file Form 5405. The 15-year repayment period for homes purchased in 2008 began with your 2010 tax return and ends with your 2024 tax return. 2023 You must file Form 5405 with your 2023 tax return if you purchased your home in 2008 and you meet either of the following conditions. You disposed of it in 2023. You ceased using it as your main home in 2023. Lacerte Info – how to enter |

| 5498 – IRA Contributions | IRA /Roth Worksheet (look for and enter contributions) Flow to 1040, Sch 1, p2, line 20 NOTE: Do not make entries on a Form 1099-R in the program unless you received a 1099-R from the payer. If you rolled money from a 401(k) to an IRA, you may receive a Form 5498 from the NEW trustee, and a 1099-R from the OLD trustee. Just enter the 1099-R data, not the 5498 data. You will enter the data from the Form 1099-R and the amount of the distribution that was rolled over. If 5498 received after taxes filed, just make sure numbers on 5498 matched what you reported on your taxes. ——LACERTE—— 24 (Adjustments to Income) |

| 5498 – SEP Contributions | 1040, sch 1, p2, line 16 Current Tax Year 5498 Form This form shows what person has already contributed to their SEP. The contribution shows amount with the current tax year, but amount is for the previous tax year. For Example: Tax year 2023, 5498 statement show SEP contribution of $30,000. However, the $30,000 is for tax year 2022. So, you need to calculate how much person can contribute for tax year 2023. Inform person of the amount, and make sure person makes the payment. If they do not make the payment, remove amount from SEP contribution. If you do not remove amount, person has incorrect income adjustment on 1040, p1, line 10. ATX Calculation – Calculate Amount Client can Contribute to SEP IRA – 1040, sch 1, p2, line 16; click arrow – Filer and/or Spouse column, select 2-SEP for “Compute maximum allowable contribution” – Make sure client makes the contribution before filing their taxes. If client does not make the contribution, then remove this amount from taxes. Lacerte Calculation – Calculate Amount Client can Contribute to SEP IRA – 24 (Adjustment to Income) – Section = SEP, Simple, Qualified Plans – Self-employed SEP = enter 1 for system to calculate maximum amount – If tax payer can contribute, amount shows on 1040, sch 1, p2, line 16 |

| 5498 – Re-characterize | Form 1099-R, Enter Gross Distribution in Box 7; Code is R |

| 5498-SA | Form 8889 Flow to 1040, Sch 1, p2, line 13 Contributions made to health savings account (HSA) Note: Distribution from HSA is form 1099-SA 1099-SA worksheet – distributions from health savings account (HSA) Note: Contributions to HSA is Form 8889 (Flow to 1040, Sch 1, p2, line 13) ——LACERTE—— Info 1. 32 (Health Saving Account) 2. Section Contributions and Deductions, enter info |

| 5695 Residential Energy Tax Credit 3800 General Business Credit | Residential Energy Tax Credit – Solar Panels: 5695, P1, Line 1; andP2, Line 17a, b, c – Energy Efficient Windows: 5695, P2, Line 19d Flow to 1040, Sch 3, Line 5 NOTE: Check Contract, can only Deduct Solar Items; ex: solar, sunlight power. Cannot deduct ducts redo, attic fans, window tinting/film Form 5695 | Instructions | IRS FAQs 1 | IRS FAQS 2 IRS Website, EnergyStar.Gov – find rebates and more info Includes solar, appliances, home, commercial, etc. 2024: IRS Info. Can deduct 30% of installation costs (equipment + labor) IRS Credit Max Info a. max of $1,200 for insulation material, exterior doors, windows & skylights b. annual max $2,000 for heat pumps, water heaters, biomass stoves, miomass boilers 2023: Can deduct 30% of installation costs (equipment + labor) Energy Credit – Residential and Commercial The Inflation Reduction Act of 2022 provides federal tax credits that empower Americans to make homes and buildings more energy-efficient to help reduce energy costs while transitioning to cleaner energy sources. Home Owners … New federal income tax credits for energy efficiency home improvements are available through 2032. … Up to $3,200 annually to lower the cost of energy efficient upgrades by up to 30 percent. … Upgrades such as heat pumps, heat pump water heaters, insulation, efficient doors and windows, electrical panel upgrades, home energy audits and more, are covered by these new tax credits. Home Builders … The Inflation Reduction Act of 2022 updates and extends the Section 45L Tax Credit for Energy Efficient New Homes. … For homes and units acquired on or after January 1, 2023, the base level tax credit for home builders will be specifically tied to ENERGY STAR certification for single-family, manufactured, and multifamily homes. This tax credit has been extended through 2032. Commercial Building Owners … The Inflation Reduction Act of 2022 extends and expands the energy efficient commercial buildings deduction that was made permanent under Section 179D in 2021. … Buildings that increase their energy efficiency by at least 25 percent will be able to claim this deduction, with bonuses for higher efficiency improvements. |

| 5695 Energy Credit FAQ Solar Tax Credit Solar Credit | 1. Roof Repairs and Replacments. IRS Info. Are NOT covered by Federal Solar Tax Credit, unless it assists with generating electric. a. Per IRS – In general, traditional roofing materials and structural components do not qualify for the credit. However, some solar roofing tiles and solar roofing shingles serve as solar electric collectors while also performing the function of traditional roofing, serving both the functions of solar electric generation and structural support and such items may qualify for the credit. Components such as a roof’s decking or rafters that serve only a roofing or structural function do not qualify for the credit. |

| 7203 | Used by S-Corp shareholders – to figure the potential limitations of their share of the S corporation’s deductions, credits, and other items that can be deducted on their individual returns. Effective for 2021, IRS requires S corporation shareholders to prepare and attach Form 7203 to the taxpayer’s Form 1040 to track and report stock and debt basis |

| 8606 – Nondeductible IRAs This form is not just for reporting nondeductible contributions to traditional IRAs. You also use it to report other IRA-related transactions where the government needs to track the status of your money—whether it’s been taxed or not taxed. | Use Form 8606 1. To report any money you contribute to a traditional IRA that you do not deduct on your tax return. Also called “nondeductible contributions”. Reporting it saves you money down the road. That’s because no individual’s money is supposed to be subject to federal income tax twice. Form 8606 gets it “on the record” that a portion of the money in your IRA has already been taxed. Later on, when you take distributions, a portion of the money you get back will not be subject to income tax. 2. When you take distributions from a Roth IRA 3. When you take distributions from a traditional, SEP or SIMPLE IRA at any time after you have made nondeductible IRA contributions. 4. When you Convert a traditional, SEP or SIMPLE IRA into a Roth IRA File Form 8606 …For every year you contribute after-tax amounts (non-deductible IRA contribution) to your traditional IRA …For every year you receive a distribution from your IRA as long as you have after-tax amounts, including after-tax rollover amounts from traditional, SEP, or SIMPLE IRA plans. You can file Form 8606 for Prior Years …The penalty for late filing a Form 8606 is $50. …There is no time limit for the amended/late filing. However, if a filing omission resulted in an immediate tax consequence (like the full taxation of a Roth conversion), the amendment must be made prior to the three-year limitation on refunds. |

| 8880 – Retirement Savings Credit Savers Credit Savers Tax Credit IRS Form 8880 | IRS Guidelines Credit for Qualified Retirement Savings Contributions Let’s you take a credit for saving for retirement. This credit can be claimed in addition to any IRA deduction that you claimed on Schedule 1 (Form 1040), line 20. 8880 flow to 1040, Sch 3, p1, line 4 Note: must have taxable income to get credit 2024 AND 2023 – Guidelines: 1. Max credit on tax return is $2,000 married filing joint; $1,000 all others. This is a nonrefundable tax credit (however, it can lower your tax bill.) 2. Max contribution amount that count toward saver’s credit. $4,000 married filing joint; $2,000 all others 3. Depending on adjusted gross income, credit amount is 50%, 20% or 10% of the contribution made; with max as listed in #1. … Eligible 1. Must contribute to retirement plan. Cannot be rollover contribution. 2. Age 18 or older, 3. Not claimed as a dependent on another person’s return, and 4. Not a student … Income limits – see IRS website 2022 – Who Qualifies: … Anyone who contributed to a retirement plan AND meet income guidelines … Income limits: Income from Form 1040, 1040-SR, or 1040-NR, line 11, cannot be more than; $34,000 Single; $51,000 if head of household; and $68,000 if married filing jointly … Contribution Requirement: you must have made a contribution (other than rollover contributions) to; (a) traditional or Roth IRA; (b) elective deferrals to a 401(k), 403(b), governmental 457(b), SEP, SIMPLE, or to the federal Thrift Savings Plan (TSP); (c) voluntary employee contributions to a qualified retirement plan, as defined in section 4974(c) (including the federal TSP); (d) contributions to a 501(c)(18)(D) plan; or (e) contributions, as a designated beneficiary of an ABLE account, to the ABLE account, as defined in section 529A. — Non Refundable credit. However, it does lower your tax bill. ——LACERTE—— Suppose to auto create, based on info entered. Lacerte will typically generate this credit automatically based on your IRA contribution entries in Screen 10, Wages, Salaries, Tips, Screen 13.1, Pensions, IRAs (1099-R), and Screen 24, Adjustments to Income. If your client meets all the conditions for the credit, but the form isn’t generating, make sure that your inputs are marked accurately as Taxpayer or Spouse. Additionally, if the credit is being reduced by a pension distribution on line 4, see Form 8880 Not Generating Credit Due to Pension Distributions in Lacerte. |

| 8938 | Statement of Specified Foreign Assets (need to investigate further) |

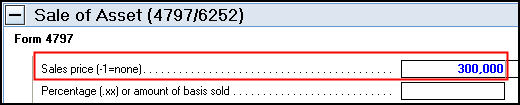

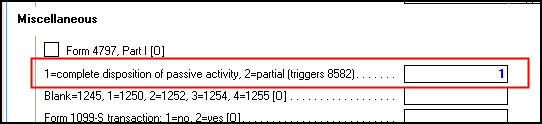

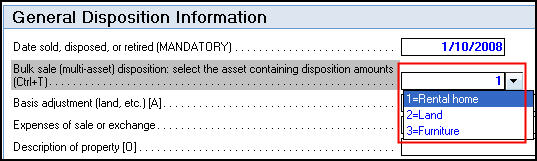

| 8949 vs 4797 8949 A= short term, basis reported B= short term, basis not reported C= short term, not received D= long term, reported E= long term, not reported F= long term, not received | info 8949 – Sales and Other Dispositions of Capital Assets. Form 8949 is for gains/losses on personal property. Property is not for producing income. 4797 – Sale of Business Property Form 4797 is for property used for business purposes, which is for producing income Part I — Sales or Exchanges of Property Used in a Trade or Business and Involuntary Conversions From Other Than Casualty or Theft—Most Property Held More Than 1 Year. Part II — Ordinary Gains and Losses. This section is for property held for a year or less. Part III — Gain From Disposition of Property Under Sections 1245, 1250, 1252, 1254, and 1255. This section is used to calculate the gain on specific types of properties as listed in the section title. Part IV — Recapture Amounts Under Sections 179 and 280F(b)(2) When Business Use Drops to 50% or Less. This is the shortest section on Form 4797. It is self-explanatory and only applies to property types for Sections 179 and 280F(b)(2). Examples: 1. Sell of your personal residence is reported on 8949. 2. Sell of a rental property is reported on form 4797 3. Sell of land that was held for investment only and not for production of income, is reported on form 8949. 4. Sell of stocks, bonds, etc are reported on form 8949. ——LACERTE—— 1. 4797, line 8 IRC 1231 loses enter in 17, select description/property, then in left panel click “Carryover/Misc”, enter info in section Form 4797, field Net Section 1231 Losses 8949: Accrued Market Discount 1. 17 (Dispositions), bottom left menu click Schedule D |

| 8958 | Allocation of Amounts Between Certain Individuals in Community Property States Complete for Married Filing Separate and person(s) live in community property state – ex California ——LACERTE—— 1. Go to 3.1 (Community Property Income Allocation) 2. Complete for the different income i.e., wages, interest income, dividends, state income tax refund,… |

| 8960 | Net Investment Income Tax – Rate is 3.8% on certain net investment income of individuals, estates and trusts that have income above the statutory threshold amounts. – Includes interest, dividends, capital gains, rental and royalty income, non-qualified annuities, etc. – Not included, wages, unemployment compensation, Social Security Benefits, alimony, and most self-employment income. |

| 8995 vs 8995-A | Both are for qualified business deduction. – 8995 is the simplified form, only one page. – 8995-A is complex form, two pages, four section. you calculate phase-in/out deductions; plus other calculations. |

| 8995 – Qualified Business Income Deduction (QBI) | Flow to 1040, line 13 qualified business income deduction Lacerte Info how enter and calculate QBI See also info 2024 – QBI Deduction Info 2023 – who can take deduction | IRS Info Where owners of pass-through entities—sole proprietorships, partnerships, LLCs, or S corporations—use to take the qualified business income (QBI) deduction, also known as the pass-through or Section 199A deduction. – Pass through income is business income that you report on your personal tax return. – Qualified Business Income means your business’s net profit. – Business owners can deduct up to 20% of their qualified business income. – 2023: Total taxable income (this is not just your business income but other income as well) in 2023 must be under $182,100 for single filers or $364,200 for joint filers to qualify. – 2024: In 2024, the limits rise to $191,950 for single filers and $383,900 for joint filers. – If you’re over that limit, complicated IRS rules determine whether your business income qualifies for a full or partial deduction. – Not all business income qualifies. QBI excludes: a. Capital Gains or Losses, b. Dividends, c. Interest Income, d. Income earned outside U.S., e. certain wage and guaranteed payments made to partner and shareholders – If your total QBI is less than zero, you must carry the loss forward into the next tax year. |

| Adoption | Form 8839, flow to Schedule 3, line 6c IRS Info Lacerte – Screen 37 – Get Credit for qualified adoption expenses paid to adopt an eligible child. It is a non-refundable credit. However, credit in excess of your tax liability may be carried forward for up to file years. – Exclude from income any employer-provided adoption assistance. Eligible Child – An individual who is under the age of 18 or is physically or mentally incapable of self-care Qualified Adoption Expenses 1. Reasonable and necessary adoption fees 2. Court costs and attorney fees. 3. Traveling expenses; including meals and lodging while away from home 4. Other expenses directly related to and for adopting a child 2024 Tax Credit a. max credit $16,810; b. phase out at modified adjusted gross income > $252,150 c. complete phase out at modified adjusted gross income > $292,150 2023 Tax Credit a. max credit $15,950; b. phase out at modified adjusted gross income > $239,230 c. complete phase out at modified adjusted gross income > $279,230 2022 Tax Credit a. max credit $14,890 b. phase out at modified adjusted gross income $223,410 c. complete phase out at modified adjusted gross income $263,410 Special Needs Adoption / Adoption from Foster Care For Adoptions, Special Needs does not mean disabled. Generally, “special needs adoptions” are the adoptions of children whom the state’s child welfare agency considers difficult to place for adoption. 1. You are eligible for the maximum amount of credit in the year the adoption became final for each adopted child. 2. You can claim max credit even if you had little or no adoption expenses. However, Max credit will be reduced by any qualified adoption expenses you claimed for the child in prior years. Note: you only get max credit; not max credit plus adoption expenses. 3. Modified Adjusted Gross Income Apply A child has special needs for purpose of the adoption expenses if: 1. Child is a citizen or resident of the United States or its territories when the adoption effort began; 2. A state determines that the child can’t or shouldn’t be returned to their parents’ home; and 3. The state determines that the child probably won’t be adoptable without assistance provided to the adoptive family. |

| Adoption California | Form 540, line 43 or 44 California Info 2024 AND 2023 Tax Credit – California If you adopted a child in California you can claim a credit for 50% of the cost. – Max deduction is $2,500 per child in a tax year. – If your costs were more, carry over the extra credit to future years until the credit is used. |

| Alimony | Alimony Paid — 1040, Sch 1, p2, line 19 Alimony Received — 1040, Sch 1, p1, line 2a Can You Deduct OR Must You Report Alimony Payment 1. Support Order AFTER 1/1/2019 – If your first spousal support order or judgment was completed on or after January 1, 2019: Federal income taxes = you cannot deduct the payments made AND you do not report payments received as income on taxes. State Income taxes = California law differ from Federal. You can deduct payments made AND you must report payments received as income on California taxes. 2. Support Order BEFORE 1/1/2019 – If your first spousal support order or judgment was completed before January 1, 2019: Federal and California are the same. You can deduct payments made AND you must report payments received as income on federal and state taxes. ——Lacerte—— Alimony Paid = 24, section = Alimony Paid, enter in Alimony paid Alimony Received = 14, section =Alimony and Other Income, enter in Alimony received |

| Alternative Minimum Tax (AMT) | Form 6251, Flow to 1040, Schedule 2, page 1, line 1 info on AMT ——LACERTE—— Force Print Alternative Minimum Tax 1. 40 (Alternative Minimum Tax 6251) 2. Scroll to bottom, field 1=Force Form 6251…, enter 1 |

| Amend Return – ATX | atx support Enter Original Return, if not in system; then select Amend Federal = 1040X; CA = CA SCHX Can adjust amount paid with extension Refund – Federal, cannot do direct deposit of refund – CA, you can direct deposit refund Create and e-filing form 1040X. 1. Open the original return 2. Click the Returns menu, then select Amend Return 3. The amendment form is installed to the return and opens the return. 4. Make changes 5. Be sure to add explanation on page 2 6. Save 7. Click e-file, Create E-file. |

| Amend Return – LACERTE | Individual Return | for other types | Trust Return Individual (screen 59) Partnership (screen 70) S-Corporation (screen 79) Corporation (screen 55) Exempt Organization (screen 74) Fudiciary (screen 74) Individual Return (screen 59) 1. Copy existing return, name file AMEN9999 2. Open return you just copied (AMEN9999) 3. Go to Screen 59, Amended Return (1040X) 4. Select returns to amend (federal/state) from the drop down in Federal/State return(s) to amend (Ctrl+T) (MANDATORY) and select OK to continue. 5. Select year to amend 6. Verify the time and date listed in the information window, then select OK. 7. Lacerte will automatically bring over original amounts from the return into the Original Amounts column on this screen. If the amounts don’t auto-populate, make sure the F4 status of the return isn’t marked as Return Complete. 8. Enter reason for amend in Section =Explanation of changes Remember to enter reason for amending 9. Use the primary input screens to make the necessary corrections to the return. For example, if you’re amending to report additional wages, go to Screen 10, Wages, Salaries, Tips to correct the wage amount. – Use the Forms tab to review the 1040X for accuracy. Refund for Amended Return – Federal, cannot do direct deposit of refund – California, you can direct deposit refund |

| Amend Return California – ATX | CA Info for 2022 For other years search: California 2020 Instructions for Schedule X (change 2020 to year you want) Individual filing amended personal return, use Schedule X; attach Schedule X to your completed amended tax return. Attach to amended tax return: – Federal schedules if you made a change to your federal tax return. – Documents supporting each change, such as corrected federal Form(s) W-2, Wage and Tax Statement, or 1099, California Schedule(s) K-1, Share of Income, Deductions, Credits, etc., escrow statements, court documents, contracts, etc. |

| Assembly Return | Individual (1040) Corporation (1120) Partnership (1065) Estates (1041) |

| Balance Sheet | The balance sheet (Schedule L) and Schedule M-1 is required if the corporation’s total receipts (gross income / sales) for the tax year and its total ending assets are more than $250,000. |

| Bonus Contribution | Bonus Contributions means amounts contributed to the Plan by the Employers. Bonus Contributions are part of the ESOP (Employee Stock Ownership Plan). |

| Business / Short-Term Rentals | Sch C, flow to 1040 line 8 (or 1040, Sch 1, p1, line 3) If Taking Depreciation If your short-term rental only averages 30 days or less as an average rent period, it would classify as transient. It is therefore classified as a commercial property and depreciates over 39 years. |

| Business Taxes | IRS Info 1. Income Tax All businesses except partnerships must file an annual income tax return. Partnerships file an information return. 2. Estimated Taxes Generally, you must pay taxes on income, including self-employment tax, by making regular payments of estimated tax during the year. 3. Self Employment Tax Self-employment tax (SE tax) is a social security and Medicare tax primarily for individuals who work for themselves. Your payments of SE tax contribute to your coverage under the social security system. Social security coverage provides you with retirement benefits, disability benefits, survivor benefits, and hospital insurance (Medicare) benefits. Generally, you must pay SE tax and file Schedule SE (Form 1040 or 1040-SR) if either of the following applies. — If your net earnings from self-employment were $400 or more. — If you work for a church or a qualified church-controlled organization (other than as a minister or member of a religious order) that elected an exemption from social security and Medicare taxes, you are subject to SE tax if you receive $108.28 or more in wages from the church or organization. 4. Employment Taxes When you have employees, you as the employer have certain employment tax responsibilities that you must pay and forms you must file. Employment taxes include the following: — Social security and Medicare taxes — Federal income tax withholding — Federal unemployment (FUTA) tax 5. Excise Tax You may have to pay and file the forms if you do any of the following. — Manufacture or sell certain products. — Operate certain kinds of businesses. — Use various kinds of equipment, facilities, or products. — Receive payment for certain services. |

| CA 565 vs CA 568 | CA 565 – Return of Partnership Income – File by Partnership Filed by a partnership (including REMICs classified as partnerships) that engages in a trade or business in California or has income from a California source must file Form 565. LLCs Classified as Partnerships File Form 568 LLCs classified as partnerships should NOT file Form 565, Partnership Return of Income. CA 568 – Return of Limited Liability Income – File by LLC Form 568 must be filed by every LLC that is not taxable as a corporation if any of the following apply: The LLC is doing business in California. The LLC is organized in California. |

| California Adjustments | While the Tax Cuts and Jobs Act (TCJA) eliminated various deductions, California Not Confirm – Allows (and not allow) Deducting the following 1. Business can NOT take Section 199A, Qualified Business Income (QBI) 20% deduction 2. State and Local Tax deduction can exceed $10,000 3. Unreimbursed employee business expenses are allowed 4. Employee Moving expenses allowed (Form FTB 3913) 5. Miscellaneous Expenses allowed include: a. Investment Advisory and Management fees b. Legal and Tax Advice fees c. Trust Fees to manage IRAs and other investment accounts d. Safe Deposit box rental fees e. Tax Prepare Fees 6. Alimony Payments – taxable to individual receiving alimony payments, and person making alimony payments can deduct payments as an “above the line” adjustment to income 7. Mortgage Interest – allow deductions for home mortgages up to $1 million plus up to $100,000 in equity debt, regardless of date purchased. (TCJA limits to $750,000, depending on date purchased) 8. Cannabis Business – between 1/1/2020 and 1/1/2025 If licensed, cannabis business can deduct ordinary and necessary business expenses on California return. If not license, business can NOT take deductions; they can deduct cost of goods sold. California Conform / Agree with TCJA on following 1. Medical Expense must be 7.5% of adjusted gross income 2. ABLE program (Achieving a Better Life Experience) 3. Cannot deduct Business Entertainment Expenses 4. Can exclude Student Loan Debt Cancellation from taxable income, if for profit school closed 5. many other areas |

| Capital Gain / 1099-B | Form 8949, flow to Sch D for State: CA, flow to CA sch D (540) |

| Capital Loss Carryover | Schedule D | Sample Carryover Schedule D | Sample 2 Capital Losses flow to 1040, line 7 State: Sample ATX: CA Sch D 540, tab= Cap Loss Co (next year) – Max allowed to deduct each year is $3,000 – Use Short-term Carryover amount first, then long-term amount – Capital losses that exceed capital gains in a year may be used to offset ordinary taxable income up to $3,000 in any one tax year. Net capital losses in excess of $3,000 can be carried forward indefinitely until the amount is exhausted. Get Remaining Balance / Next Year Carryover Info ATX: Sch D, tab= Cap Loss Co (Next Year) Lacerte: 17 (dispositions), click button Carryover/Misc Calculate Carryover Loss using amounts on Schedule D – amount must be negative to be a loss carryover – positivie amount is NOT a loss carryover – you subtract 3,000 to get amount; since loss is negative, you add 3,000 1. Short-Term Carryover = line 7 amount +3,000 2. Long-Term Carryover = line 15 amount +3,000 Enter Carryover Info – Lacerte Instruction on Different Types of Returns 1. Individual Return: 17, Section Dispositions, click button “Carryovers/Misc”, enter info in Schedule D – Capital Loss Carryover |

| Cancellation of Debt (Debt Cancellation) | Client receives 1099-C 1040, p1, line 8, click arrow, line 8c, click arrow, 8c (or can enter on line 8z) or, 1040, Sch 1, p1, line 8c, click arrow, 8c Exclusion for Qualified Principal Residence 1. Provide tax relief on canceled debt for homeowners involved in mortgage foreclosure 2. Allow taxpayer to exclude up to $2,000,000 for married filing joint; $1,000,000 all others 3. Under Consolidated Appropriations Act of 2021, congress retroactively extended from 2018 through 2025 tax year. 4. Taxpayers can exclude mortgage foreclosure debt cancellation from taxable income |

| Car Payment – Car Lease Lease Down Payment | Purchased Car 1. Cannot write off car loan payments 2. Cannot write off down payment 3. You can write off car loan interest, based on business usage % Leased Car 1. You can write off lease payment, based on business usage % 2. You can amortize lease down payment over the term (life) of lease agreement Standard or Actual Mileage Deduction Standard mileage rate is the best method when you drive a lot for work. Otherwise, actual is better. Costs not included with Standard Mileage, but can be deducted – parking fees, – tolls, – DMV fees, – car washes – etc. Changing from Standard to Actual Mileage If you use the standard mileage method in the first year, you can change to the actual expenses method the next year. However, if you use the actual expenses method the first year, you cannot change to another method in future years. |

| Car Sale | Report on Schedule D If you made a profit on the sale of your car Example: purchased car for $5,000 and sold it for $7,500; you made $2,500 profit; therefore you must report sale on taxes. Proceeds = Sale Price Cost Basis = Purchase Price + Shipping Costs + Setup Costs + Sales Tax + Improvements a. Cost Basis does NOT include regular maintenance or repairs b. And, You must subtract any sales tax refunds and manufacturer rebates From Cost Basis |

| Carryover Losses Carryforward Losses Carryback Losses Unallowed Losses Carryover Carryover Sample Carryover Example Carryover Credit Carryforward Carry Forward | – 1116 Foreign Tax Carryover a. Lacerte: 35.1 Foreign Tax Credits; Section top left, Foreign Tax Credit Carryovers b. ATX: Go to 1116, Tab =Sch B, Line 7, Current Year Carryover – 4952 Carryover – Investment Interest Expenses a. Lacerte: 25 – Itemized Deductions; Section Interest / Investment Interest Carryover – 8582 Carryover – Rental Property, Schedule E a. Lacerte: 18 – Rental (Schedule E); Section Prior Year Unallowed Passive Losses b. AT: Sch E, p1, bottom tab= click loss limitation, ck ‘X’ at top of page to enter prior year At-Risk or Passive Carryover amounts – 8829 Carryover – Business Use of Home a. Lacerte: 29 – Business Use of Home; Section Carryover of Unallowed Expenses – 8995 Carryover – Qualified Business Income Deduction a. If QBI for Rental: Lacerte: Screen 18, Section Prior Year Unallowed Passive Losses b. If QBI for Business: Lacerte: Screen 16, Section Prior Year Unallowed Passive Losses c. If QBI for K-1: Lacerte: Screen 20.1, Select K-1 Type, Section Prior Year Unallowed Qualified Business Income – K-1 1065 Carryover – Passive a. Lacerte: Screen 20.1, Select K-1 Type, Section Prior Year Unallowed Passive Losses – Partnership Basis Carryover a. Lacerte: Screen 20.1, Select K-1 Type, Section Basis Carryovers b. ATX 1. On the K-1 (1120S) or K-1 (1065) Input tab select the box at the top “Check (X) to enter prior year Passive carryover amounts”. 2. Prior year passive losses should be entered on the Input tab in the Passive Limitation section at the very bottom of the sheet. Schedule C Carryover – Business a. Lacerte: 16 – Business Income, Section Prior Year Unallowed Passive Losses – Schedule D Carryover – Capital Losses (Sample 2 | State Sample) a. Lacerte: 17.1- Dispositions; Section Carryovers/Misc Info (or click button Carryovers/Misc) b. Capital Losses flow to 1040, line 7 |

| Casualty Lost or Theft | Form 4684; flow to 1040, Sch A, line 15 for personal flow to 1040, Sch 1, line 4 or 4797 for Business / Trade Property a Total Loss If your rental property is completely destroyed or stolen, your deduction is calculated as follows: Adjusted basis – Salvage value – Insurance proceeds = Deductible loss. Your adjusted basis is the property’s original cost, plus the value of any improvements, minus any deductions you took for regular or bonus depreciation or Section 179 expensing. You determine the basis for your building, land improvements, and landscaping separately. Adjusted basis should be easily found from a rental property’s depreciation schedules and/or tax returns filed for the property. Salvage value is the value of whatever remains after the property is destroyed. This usually won’t amount to much. For example, if a rental house burns down completely, there may be some leftover bricks, building materials, personal property, and other items with some scrap value. Obviously, if a personal property item is stolen, there will be no salvage value at all. |

| Celsius Bankruptcy Digital Currency | Per Celsius Bankruptcy Order Sample Calculation | Celsius Distrubtion Effective Date 1/16/24 see page 13 | Celsius Value Time of Bankruptcy see page 5 | more info 1. Bankruptcy filed 11/21/2022 2. Persons holding coins in Celsius will value their holding based on coin worth on 7/13/2022. They can use this amount to determine their claim with Celsius. 3. Celsius Bankruptcy order issued 3 types of assets to settle claims: BTC (Bitcoin), ETH (Ethereum), and Shares of Ionic Stock. 4. Court put the Issued assets value, of the coins, based on worth on 1/16/2024; which is BTC = $42,972.9948 ETH = $2,577.4752 Ionic Stock = $20 per share |

| Charity Donations | 2024 – must itemize to get charity donation – there are no above the line deductions – limit on cash contributions is 60% of taxpayer’s adjusted gross income – appreciated assets (stock, bonds, real estate, etc.), max deduction is 30% of adjusted gross income 2023 – must itemize to get charity donation – there are no above the line deductions – limit on cash contributions is 60% of taxpayer’s adjusted gross income 2022 – must itemize to get charity donation – there are no above the line deductions -$300 or $600 married filing joint – limit on cash contributions is 60% of taxpayer’s adjusted gross income Benefits – Charity donations reduce your tax bill roughly 25 cents for every dollar donated. 50% Charities = most religious groups, schools, hospitals and public charitable organizations 30% Charities = veterans associations, fraternal organizations and cemetery organizations. Plus, Deductions for contributions of long-term capital gain property (such as appreciated securities held for more than one year) are limited to 30% of AGI. |

| Charity Donations – Non Cash > $500 | Form 8283 Make Donor Cost / adjusted basis 3.1 time fair market value |